For their successful, good life Information you really need: Government-funded publisher, awarded the Global Business Award as Publisher of the Year: Books, Shops, eCourses, data-driven AI-Services. Print and online publications as well as the latest technology go hand in hand - with over 20 years of experience, partners like this Federal Ministry of Education, customers like Samsung, DELL, Telekom or universities. behind it Simone Janson, German Top 10 blogger, referenced in ARD, FAZ, ZEIT, WELT, Wikipedia.

Disclosure & copyrights: The airline Condor is our regular cooperation partner for various research trips. Image material created by Verlag Best of HR – Berufebilder.de®. The Kenyan Tourist Board covered the cost of accommodation and food for a research trip to Kenya.

M-PESA - Kenya's pioneering role in mobile payment: driver of innovation instead of stone age village

By Simone Janson (More) • Last updated on October 05.02.2022, XNUMX • First published on 18.01.2013/XNUMX/XNUMX • So far 4389 readers, 1654 social media shares Likes & Reviews (5 / 5) • Read & write comments

Anyone who goes to Kenya will notice fast, how ubiquitous mobile payment with the mobile phone is. Unlike in Germany, where the introduction of appropriate Features has been hotly debated for years. Is Germany missing out on a trend that led to a minor economic miracle in Kenya?

Contents

Hide

- SMS payment NFC chip

- Germany: too many possibilities

- The skepticism is great

- Do not worry about data gagging

- The dilemma of saturated markets

- Above all, the banks are blocking themselves

- Kenya: The pure need as an innovation driver

- Stereotypes and reality

- Innovation instead of Steinzeitdorf

- What is M-PESA and how does it work?

- The economic miracle of Kenya

- Top books on the subject

- Read text as PDF

- Advice on success, goal achievement or marketing

- Book eCourse on Demand

- Skate eBook as desired

SMS payment NFC chip

The Kenyan mobile payment model is very simple, it works with SMS and with every mobile phone. Expensive smartphones do not need the users.

In Germany, the Industry on the other hand, on the NFCTechnology, with which far too few mobile phones are equipped. Apple's current iPhone does not have an NFC chip either. The pain threshold for retailers to introduce the necessary infrastructure is a ridiculous 5% NFC-enabled cell phone. And that threshold hasn't even been reached yet.

Germany: too many possibilities

The books on the subject (advertising)

Tip: You can also use this text as a PDF or an eCourse on the subject download. You can also find it in the shop exciting inspiration to experience your success, plus offers & news in Newsletter ! (Advertising)

The number in direct comparison to Kenya shows how much the Companys have to lower their expectations in this country - and where the rub is: There are too many competing payment systems, among which the customers can choose.

This makes it difficult for companies to establish a standard and, as a result, nobody is willing to invest in the corresponding infrastructure invest.

The skepticism is great

In addition, there is the great skepticism with which the topic is met in this country: As I was able to experience on the Omnicard, many companies do not see any in mobile payment Future; and why should he Customer prefers the plastic cards anyway.

Incidentally, the banks are at the forefront of prophecies of doom, perhaps also because they care about her Shop fear - even if the savings bank has just started a pilot project for mobile payments.

Do not worry about data gagging

Discounts for your success (advertising)!

On the customer side, however, are the security concerns, the well-known German Anxiety: Who in Germany would want to entrust their entire life to a smartphone? Around Honestly I'm skeptical about it too.

The Kenyans I spoke to, however, are not concerned about this topic - even though Vodafone has sometimes had a somewhat strange view of the Privacy noticed and also ventures far forward on the subject of net neutrality.

The dilemma of saturated markets

Overall, the example of mobile payment shows a lot clear the dilemma of a saturated market in the industrialized nations: The discussion about mobile payment methods has been going on at the Omnicard and elsewhere for 10 years, but is far too small steps Ahead.

Because there is already a good infrastructure for financial services, there is no need to introduce new payment procedures. Because the customer always chooses the payment option that seems most practical to him.

Above all, the banks are blocking themselves

Mobile payment options are due to the associated high technical effort in Germany rather not. Therefore, the demand is missing and on the contrary, in view of the competition, there is still the danger of Verzetzlung. Therefore, the companies do not move and everything stays the same.

As it also shows on the Omnicard, it is above all the banks that lock themselves. Even if the savings banks have just launched a pilot project with which they want to implement mobile payment nationwide - one might suspect they are afraid to give their market leadership in money management to mobile operators, as is the case in Kenya.

Kenya: The pure need as an innovation driver

In Kenya, with its much poorer infrastructure, customers are much more willing to accept the innovations. At the same time, operators were forced to Solution how to find payment via SMS, because more complex System wouldn't have worked at all: People just don't have one Money for expensive smartphones.

The mobile paymentIdea fell on fertile ground and thrived splendidly. As is so often the case, pure economic necessity becomes the driver of innovation, while the saturated markets have to be careful not to be left behind.

In Germany, for example, at the Smart Card Conference Omnicard in Berlin, representatives of IT and communication companies, banks and institutions spend three days discussing technical innovations such as mobile payment functions by mobile phone, which are still in their infancy in Germany. In East African Kenya, the Masai are (not only) far ahead of us.

Stereotypes and reality

So-called third partiesWelt-Countries are often seen as backwards and the Maasai, an East African nomadic people, are considered by many to be the epitome of a Stone Age nomadic way of life.

In fact, the Masai traditionally have little stone age, since they had, for example, blacksmiths and cattle. That clichés do not always have to be right, we have not known since the satirical heating collection campaign that South Africans organized for Norway.

Innovation instead of Steinzeitdorf

Because even if we have visited such a Stone Age nomadic village, Kenya as far as the mobile, cashless payment by mobile phone, far ahead of us; I was able to convince myself of that during my last visit:

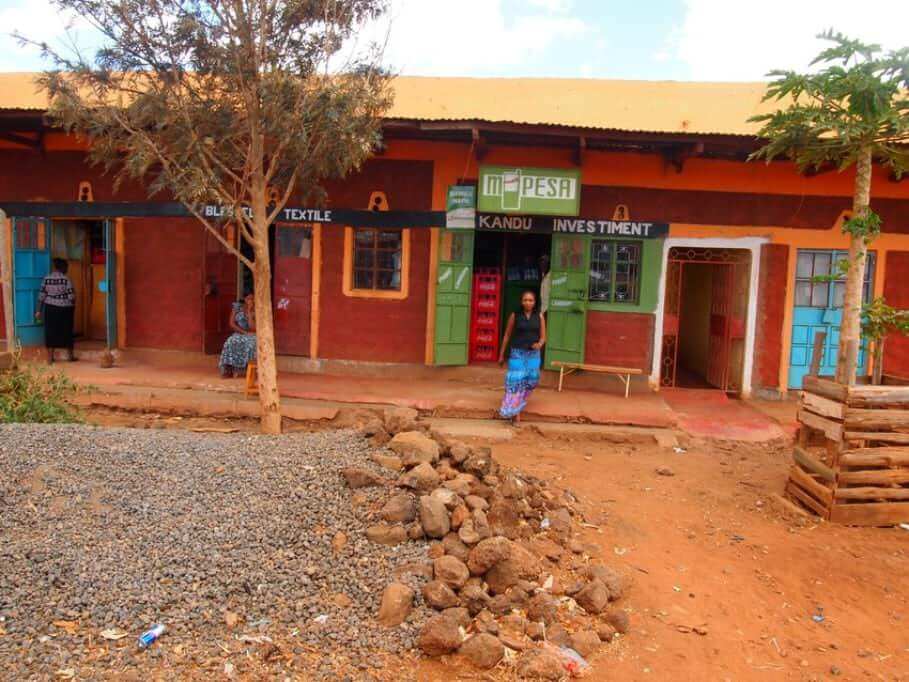

Bank vending machines or even stores are sought in vain in the vast steppe. But there are M-PESA agents in almost every settlement along the dusty dirt roads - as here in Mbirikani, which is mostly operated by Maasai.

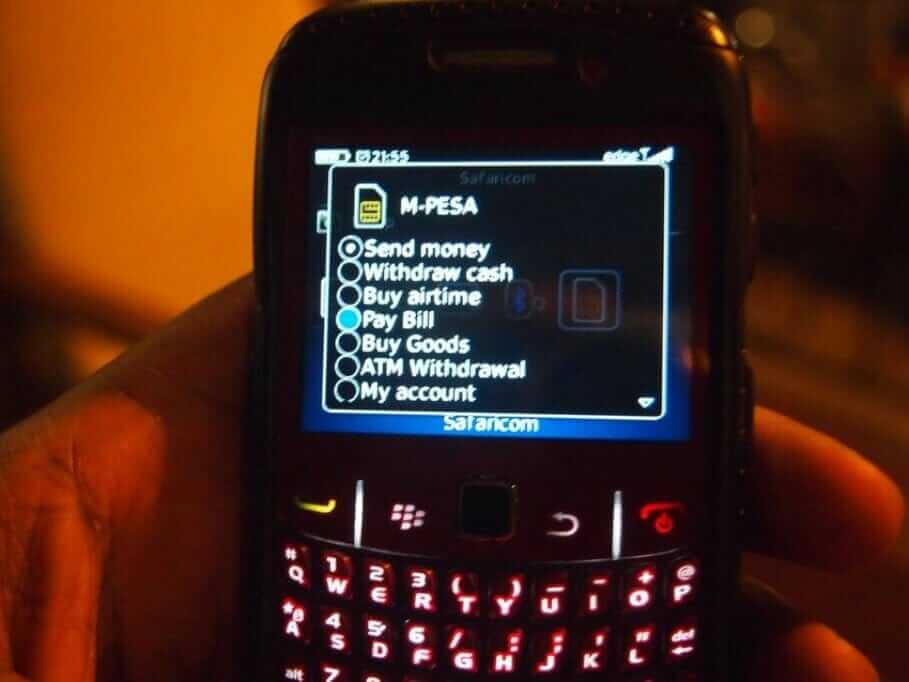

What is M-PESA and how does it work?

M-PESA was launched in Kenya in early 2007 by the Kenyan mobile operator Safaricom, now a Vodafone subsidiary. With this system, the Kenyans can perform basic functions of money transfer and private cashless payments via mobile phones without the need for a regular bank account. Uta Hergenroether describes exactly how this works in the Betterplace Lab:

“Anyone who has a cell phone or knows someone who has one and can send and receive SMS can use M-PESA. Customers who want to transfer money can register for Safaricom for the M-PESA service free of charge and adjust their SIM card. Then they receive a PIN for their telephone number, which is required for every transaction. Now you can top up money as needed and send or receive it via encrypted SMS for a small fee within your own country. The deposit and “storage” of money on the mobile phone is free of charge. So-called M-PESA, which can be full-time Internet café owners, petrol station or pharmacy owners, are used for cash payments. They paid a one-time fee to Safaricom for the operator license (and the associated IT device). There are now almost 40.000 of these agents in Kenya who also use their own cell phones to offer services to non-M-Pesa customers. ”

The economic miracle of Kenya

The ease of use (overview of all functions thanks to the very readable post including comments by Andreas Fischler) is probably the reason why, according to various media reports, an economic miracle has broken out in Kenya. The People save money and Women start a business, what a small one Revolution equals.

According to Wikipedia, M-PESA now has 15 million users, which is around 80% of mobile phone customers. Vodafone now wants to export the successful model to other countries. For comparison: only 15% of adults have a bank account at all.

Top books on the subject

Read text as PDF

Acquire this text as a PDF (only for own use without passing it on according to Terms and conditions): Please send us one after purchase eMail with the desired title supportberufebilder.de, we will then send the PDF to you immediately. You can also purchase text series.

4,99€Buy

Advice on success, goal achievement or marketing

You have Ask round to Career, Recruiting, personal development or increasing reach? Our AI consultant will help you for 5 euros a month – free for book buyers. We offer special ones for other topics IT services

5,00€ / per month Book

Book eCourse on Demand

Up to 30 lessons with 4 learning tasks each + final lesson as a PDF download. Please send us one after purchase eMail with the desired title supportberufebilder.de. Alternatively, we would be happy to put your course together for you or offer you a personal, regular one eMail-Course - all further information!

29,99€Buy

Skate eBook as desired

If our store does not offer you your desired topic: We will be happy to put together a book according to your wishes and deliver it in a format of yours Choice. Please sign us after purchase supportberufebilder.de

79,99€Buy

Here writes for you

Simone Janson is publisher, Consultant and one of the 10 most important German bloggers Blogger Relevance Index. She is also head of the Institute's job pictures Yourweb, with which she donates money for sustainable projects. According to ZEIT owns her trademarked blog Best of HR – Berufebilder.de® to the most important blogs for careers, professions and the world of work. More about her im Career. All texts by Simone Janson.

Simone Janson is publisher, Consultant and one of the 10 most important German bloggers Blogger Relevance Index. She is also head of the Institute's job pictures Yourweb, with which she donates money for sustainable projects. According to ZEIT owns her trademarked blog Best of HR – Berufebilder.de® to the most important blogs for careers, professions and the world of work. More about her im Career. All texts by Simone Janson.

Popular Posts

-

Applying chaotic time management correctly: plan & order for success?

-

Working world 4.0 & new tasks for HR: Trend Collaborative HR

-

Further education, MBA & postgraduate studies: cost-benefit calculation for lateral entry into the economy

-

Self-determined organization in the home office & on the go: 7 tips for the right mindset

-

Career entry for humanities and social scientists: practical test for graduates

-

OPINION! Jürgen Schwarz, Operations Manager at Kissel + Wolf GmbH on the shortage of skilled workers, googling applicants & the AGG: “Many applicants destroy their own job market”

-

The role of social media managers: The battle is not over yet!

-

Decide really well & motivated: Logical vs. conservative

4 responses to "M-PESA - Kenya's pioneering role in mobile payment: innovation driver instead of Stone Age village"

-

In fact, Germany is a developing country when it comes to this topic.

-

Sometimes I can't click the menu on your site - why is that?

-

That this article has not been commented yet, clearly shows that in Germany far too much is accepted as an alternative. Too few think about new ways. Here financial service providers could be hit, in which strong competition arises.

-

Hello Taxforce,

that is precisely the point that the banks here want to secure their benefices. But also the concerns of the customers and eg of the retail trade are great: In many restaurants and even in the supermarket you can not pay with 5 or 10 euros with a card, because the company costs too much.

-

Post a Comment