Your shopping cart is currently empty!

For their successful, good life Information you really need: Government-funded publisher, awarded the Global Business Award as Publisher of the Year: Books, Magazine, eCourses, data-driven AI-Services. Print and online publications as well as the latest technology go hand in hand - with over 20 years of experience, partners like this Federal Ministry of Education, customers like Samsung, DELL, Telekom or universities. behind it Simone Janson, German Top 10 blogger, referenced in ARD, FAZ, ZEIT, WELT, Wikipedia.

Disclosure & Copyrights:

Disability Insurance: Abstract Reference Dread Disease Alternatives & Self Employed

By Simone Janson (More) • Last updated on October 22.10.2009, XNUMX • First published on 22.10.2009/XNUMX/XNUMX • So far 7325 readers, 4795 social media shares Likes & Reviews (5 / 5) • Read & write comments

If you want to take out disability insurance, you have to take a few things into account - including the abstract reference and exceptions for the self-employed. Well therefore if it too Alternatives like dread disease insurance.

Contents

Hide

- Abstract reference

- Dread disease insurance

- Services and alternatives

- Basic ability insurance

- Disability Insurance

- Life Insurance

- Is burnout a case for disability insurance?

- The judgment

- Why burnout?

- What self-employed have to consider

- Top books on the subject

- Read text as PDF

- Advice on success, goal achievement or marketing

- Book eCourse on Demand

- Skate eBook as desired

Abstract reference

The books on the subject (advertising)

Tip: You can also use this text as a PDF or an eCourse on the subject download. You can also find it in the shop exciting inspiration to experience your success, plus offers & news in Newsletter ! (Advertising)

If your insurance contract contains wording such as “…if the insured person is unable to Job or to engage in any other activity that he is required to do on the basis of his Vocational Training and experience and which corresponds to his previous position in life” contains: Keep your hands off it. It is a so-called abstract reference.

That means you from the Insurance no Money as long as you can still carry out such an activity, even if you could only theoretically carry out the other work, but in practice there is no need for your (health-impaired) workforce and you therefore cannot find a job.

According to current case law, a job that corresponds to your previous position in life can also mean that you get 20 percent less to earn. In contrast to older contracts, however, most newer contracts usually do not contain such references.

Dread disease insurance

If you opt out of disability insurance decide, because the conditions seem too unfavorable to you or if the insurance company has rejected your application, you do not have to do without private insurance cover, because there are still some alternatives: For example, dread disease insurance.

The Term “Dread Disease” comes from English and means something like “serious illness”. The Performance From this insurance is usually a one-time sum of money. It is paid if one of the contractually defined illnesses occurs. Because even if there is no occupational disability, a serious illness often leads to a permanent limitation of personal performance.

Services and alternatives

Discounts for your success (advertising)!

What a dread disease insurance actually provides depends on the tariff of the individual provider. Every Society insures different diseases. In general, diseases such as cancer, heart attack, stroke - including bypass operations - are included in the insurance cover. Basically, the more illnesses are included, the higher the insurance premium. If one of these diseases then occurs, a previously agreed sum insured is due. Since this is usually a one-off payment, dread disease insurance can also be a useful supplement to an occupational or disability pension.

In addition to Dread Disease insurance, there are other alternatives to occupational disability insurance: namely basic and disability insurance.

Basic ability insurance

The basic skills insurance pays a monthly fee in the event of the loss of certain skills pension. All abilities that are insured are listed in the contract – such as seeing, driving a car or grasping.

If the insured person is no longer able to carry out these activities as a result of illness, bodily injury or loss of power, the insurer shall do so. A prerequisite for this is a medical assessment which indicates that the person concerned has been or is not capable of performing at least one of the activities specified in the contract for at least twelve months.

Disability Insurance

Disability insurance serves as protection in the event that you are no longer able to carry out any activity regularly and permanently. It is similar to the statutory disability pension. Unlike an occupational disability insurance, the previously practiced profession has none Significance, nor what has been achieved so far Income.

A disability insurance is therefore also significantly cheaper than a disability insurance. The following also applies to disability insurance: It is offered as a self-employed insurance or as supplementary insurance in conjunction with a pension, endowment, life insurance or term life insurance.

Life Insurance

Even life insurance has its pitfalls. The Manager Magazin reports: Anyone who registers with the selection Capital educational life insurance beforehand, may pull a long face at the end of the contract. Because when the policy expires, his life insurer may transfer up to 30 percent less money than the best of the Industry do. This emerges from the latest double study by the industry service Map-Report.

Map-Report identified twelve high-performing and twelve less powerful insurers. The study belongs to the first group Companys Allianz Leben, Asstel, Cosmos, Debeka, DEVK aG, Hannoversche, HUK-Coburg, LV 1871, Neue Leben, R + V, Süddeutsche and Volkswohl-Bund. The second dozen of the less good insurers are the following providers: AachenMünchener, Axa, Bayern-Versicherung, Deutscher Herold, Gerling, Hamburg-Mannheimer, Iduna, Nürnberger, Provinzial Nordwest, SV Sparkassenversicherung, Victoria and Volksfürsorge. The comparative analysis is based on the development of certain characteristics such as market share, Costs (for closing and administration), net return and maturity benefits for the years 1994 to 2005.

After all, it is characteristics like this that decide how much money you have Customer finally figured out. So look carefully.

As the Strategy the magazine recommends “always seeing acquisition cost ratio and market share development as a unit. If an insurer's acquisition cost ratio is well above the market average and it is still losing market share, then this is a sign that something is wrong in sales or with the company's strategy. If at the same time the cancellation rate of a company is permanently above the market average, then the chance of permanent customer satisfaction is low. Then the high acquisition costs are probably poorly invested. That should also interest the shareholders of the life insurer.

Is burnout a case for disability insurance?

On March 22, 2006, after a three-year legal dispute, the district court in Munich issued a model judgment on the subject Burnout and mental illness like: Accordingly, the burnout syndrome clear classified as an insured event.

The judgment

A manager filed a lawsuit after a doctor confirmed that he was unable to work, but the insurance company refused to pay. At the end of 2001 he collapsed due to nervous stress and gave up his job on medical advice.

Mitfugundrecht is to be read as a comment to the judgment:

The Munich Court of Justice I had to decide whether the burn-out syndrome was reason for disability and, after obtaining a medical opinion, condemned the insurance company to reimburse 148.000 Euro disability benefits and 65.000 Euro in insurance contributions. It was not until the appeal proceedings before the Oberlandesgericht in Munich that the insurance broke up.

Why burnout?

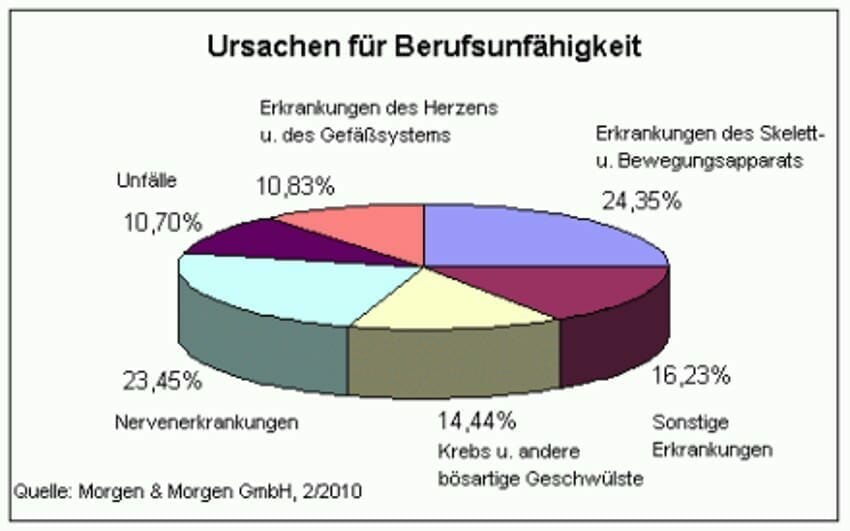

It is clear once again that mental disorders and nervous Problems are increasingly a case for disability insurance. A study by Morgen und Morgen even shows that it is the second most common cause of disability.

The fact that burnout is recognized as the cause of occupational disability is positive on the one hand, but also on the other negative, because now many insurance companies will take a closer look at previous mental illnesses before taking out disability insurance.

What self-employed have to consider

Special provisions apply to the self-employed with employees when taking out occupational disability insurance. For them, the "profession" is not just about the activity that they do themselves. It is also checked whether you are certain after an illness or an accident Tasks could delegate.

Such a reorganization of the business should be expected of a self-employed person under the following conditions: You must continue to have a meaningful workspace (not a casual job) that matches your knowledge, skills and workforce and your position as a farmer.

In addition, the reorganization must be spatially possible and not entail significant financial losses or investments. In an emergency, however, you must prove that reorganization is out of the question (e.g. because of your Health). The general economic Risks is not taken into account.

Top books on the subject

Read text as PDF

Acquire this text as a PDF (only for own use without passing it on according to Terms and conditions): Please send us one after purchase eMail with the desired title supportberufebilder.de, we will then send the PDF to you immediately. You can also purchase text series.

4,99€Buy

Advice on success, goal achievement or marketing

You have Ask about career, Recruiting, personal development or increasing reach? Our AIAdviser helps you for 5 euros a month – free for book buyers. We offer special ones for other topics IT services

5,00€ / per month Book

Book eCourse on Demand

Up to 30 lessons with 4 learning tasks each + final lesson as a PDF download. Please send us one after purchase eMail with the desired title supportberufebilder.de. Alternatively, we would be happy to put your course together for you or offer you a personal, regular one eMail-Course - all further information!

29,99€Buy

Skate eBook as desired

If our store does not offer you your desired topic: We will be happy to put together a book according to your wishes and deliver it in a format of yours Choice. Please sign us after purchase supportberufebilder.de

79,99€Buy

Here writes for you

Simone Janson is publisher, Consultant and one of the 10 most important German bloggers Blogger Relevance Index. She is also head of the Institute's job pictures Yourweb, with which she donates money for sustainable projects. According to ZEIT owns her trademarked blog Best of HR – Berufebilder.de® to the most important blogs for careers, professions and the world of work. More about her im Career. All texts by Simone Janson.

Simone Janson is publisher, Consultant and one of the 10 most important German bloggers Blogger Relevance Index. She is also head of the Institute's job pictures Yourweb, with which she donates money for sustainable projects. According to ZEIT owns her trademarked blog Best of HR – Berufebilder.de® to the most important blogs for careers, professions and the world of work. More about her im Career. All texts by Simone Janson.

Popular Posts

-

Salary equality between men and women: wage gap larger than expected! {Trend! study}

-

Postgraduate studies: Useful or not?

-

Success of social media: 5 percent more sales? {Trend! Study}

-

Acquire & retain customers: 10 tips against customer churn

-

3 tips for agile change management in companies: Leading employees in change

-

Working out a strategy – methods & procedure: 7 steps instead of a quick shot

-

OPINION! Financial expert Stefanie Kühn: "If you want to be independent, you have to understand your investments"

-

Bad managers, good executives: With personality & empathy

Post a Comment