Your shopping cart is currently empty!

For their successful, good life Information you really need: Government-funded publisher, awarded the Global Business Award as Publisher of the Year: Books, Magazine, eCourses, data-driven AI-Services. Print and online publications as well as the latest technology go hand in hand - with over 20 years of experience, partners like this Federal Ministry of Education, customers like Samsung, DELL, Telekom or universities. behind it Simone Janson, German Top 10 blogger, referenced in ARD, FAZ, ZEIT, WELT, Wikipedia.

Disclosure & copyrights: Current Bauzinsen supported us financially. onlinekreditvergleiche.com supported us financially. Images created as part of a free collaboration with Shutterstock.

Loans & insurance for customers with risk professions: scoring as a protective factor

By Susanne Kleimst (More) • Last updated on October 23.01.2024, XNUMX • First published on 23.05.2017/XNUMX/XNUMX • So far 5312 readers, 1192 social media shares Likes & Reviews (5 / 5) • Read & write comments

People Those who work in risky occupations, such as various craftsmen, teachers or musicians, often find it more difficult to take out insurance or get a loan. If they succeed, they often have to reckon with worse conditions.

Contents

Hide

- What does scoring mean?

- Scoring as the basis for decisions

- What information is important for scoring?

- Dilemma of risk management

- Disability insurance is often difficult

- Opportunities for credit protection

- High standards of data protection

- Individual scoring of banks and insurers

- Top books on the subject

- Read text as PDF

- Advice on success, goal achievement or marketing

- Book eCourse on Demand

- Skate eBook as desired

What does scoring mean?

When assessing creditworthiness, various criteria relating to living conditions are taken into account. The scoring serves on the one hand as Information for credit and insurance brokers in order to be able to submit an individually tailored offer.

The scoring primarily serves as a protective measure for the consumer. For him, the protection of the creditworthiness is in the foreground. Especially in high-risk occupations, the Customer comprehensive advice on the possibilities of securing a loan and thus being protected from excessive financial burdens.

Scoring as the basis for decisions

The books on the subject (advertising)

Tip: You can also use this text as a PDF or an eCourse on the subject download. You can also find it in the shop exciting inspiration to experience your success, plus offers & news in Newsletter ! (Advertising)

Have since 2010 customers the right to obtain information about the data collected by SCHUFA. Various information is collected there to assess the creditworthiness and evaluated by mathematical-statistical methods:

- Information about bank accounts and credit cards

- Completed leases, loans and guarantees

- Mobile phone and mail order accounts

- Installment transactions

- Possible payment defaults

What information is important for scoring?

The risk classification by SCHUFA scoring is only a very basic, if very basic, basis for the evaluation of the creditworthiness of a customer. However, a lot of other information plays an important role. These must be ascertained by the credit or insurance adviser:

- Economic conditions

- Employer and profession

- marital status

It is advisable to take this comprehensive information into account in order to make the best possible use of the customer's financial possibilities and to submit a sensible offer. The score as the only basis is usually not meaningful enough to be objective decision to be able to meet.

Dilemma of risk management

Discounts for your success (advertising)!

In addition to the risk professions, the self-employed are also affected when it comes to finding a loan. The score should not be the only criterion for rejection here. This is specified in the Federal Data Protection Act (§ 6a BDSG). Accordingly, the score serves only as a decision-making aid, but not as a basis.

Nevertheless, the individual classification has a direct effect on the terms of the loans. For example, various financial institutions stagger their lending rates according to the amount of income. The same procedure is often used for interest rates on loans. The self-employed and freelancers in particular are at a disadvantage here, their Income is irregular and subject to certain fluctuations.

Disability insurance is often difficult

The dilemma of the risk groups is twofold: on the one hand, poorer conditions have to be accepted for loans, for example for a property. In addition, it has to Risks of a credit default are taken into account.

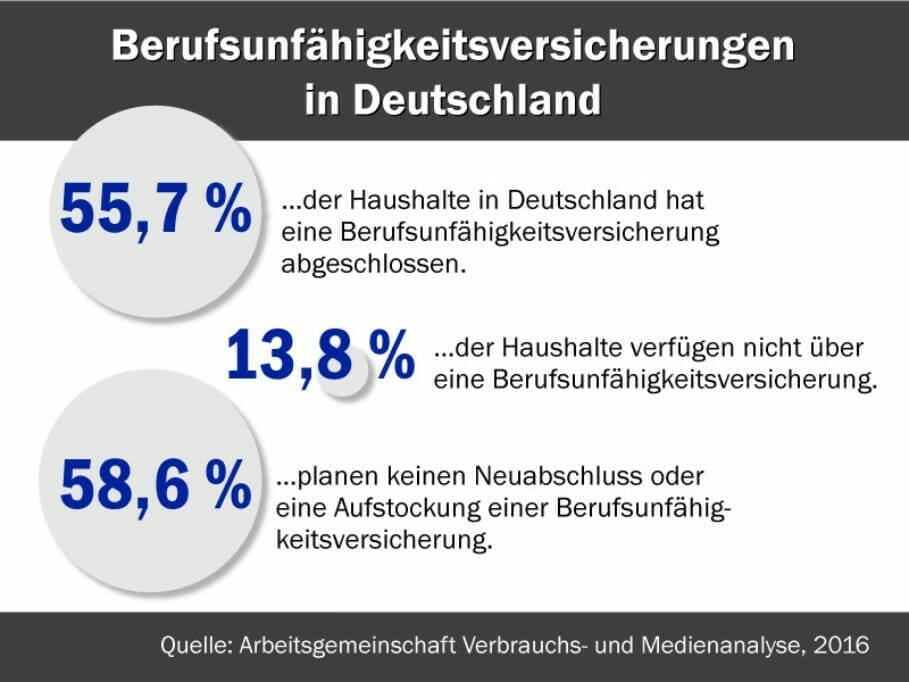

In this case, occupational disability insurance is often unaffordable or is directly rejected due to the health check. Only a little more than half of German households therefore have occupational disability insurance.

For high school graduates, this is often associated with extremely high contributions. Here it is up to the broker to inform the customer comprehensively about the risks involved in the conclusion of a loan - which, unfortunately, often happens inadequately. Above all, the loss of earnings is often treated only insufficiently.

Opportunities for credit protection

The safeguarding of a loan against payment default is an important issue, especially for risk groups, if no occupational disability insurance can be concluded at the same time. There are other possibilities:

- Alternatives to the classic BU: If disability insurance is out of the question, disability insurance is a possible alternative. However, the protection only comes into force when in fact no more work can be done. Dread disease insurance also does not offer comparable coverage, but may be able to absorb some of the loss of earnings.

- Credit protection at high values: The hedge is already included in most loans. Again, the financial service providers are based on the scores in the design of individual conditions. For long-term loans, eligible assets are often used to secure credit. As a mortgage, register deposit or collateral transfer, the values are then used as legal protection until final repayment.

- Guarantee by other persons: This option uses the good credit ratings of third parties to secure a loan. Family members or other relatives can be employed.

In addition, risk-takers in risk groups should make full use of the possibilities of the special repayment in order to be able to repay a credit agreement promptly. Above all, self-employed with fluctuating income can be at a good personal business achieve good effects with the unscheduled payments, For instance, this option should always be granted, especially for high-level loans such as real estate. Before the loan contract is concluded, the customer can discuss various cases and discuss the impact on the credit history.

High standards of data protection

The new Privacy-Basic Regulation brings on the one hand binding regulations for all member states of the EU also for scoring. On the other hand, the consumer advice center warns that the standards in the laws, which are often higher in this country, should be maintained.

In April 2016, the long-overdue European General Data Protection Regulation (DSGVO) was adopted. The growing cross-border credit and insurance market has made common rules for the individual member states urgently necessary. In May 2018 the DSGVO becomes binding for the individual countries. Up to this point in time, valid, individual data protection regulations must be adapted by the states accordingly.

In order to protect the consumers from the negative effects of scoring, the Confederation of the Consumer Center (vzbv) urges that certain stricter regulations of the German legislation be maintained. Around the current level of data protection, be it because of that usefulto transfer certain clauses into other laws.

In addition to data protection, discrimination should also be kept as low as possible. Due to the provisions of the GDPR, classifications based solely on address data should again be possible in the future. The neglect of other important influencing factors can then affect certain groups of people negative affect. Here, too, the vzbv advises to keep the current paragraph (§ 28b BDSG), which requires higher protection standards for consumers.

Individual scoring of banks and insurers

In addition to SCHUFA, many credit institutions and insurance companies have their own procedures or automated calculation procedures to classify the creditworthiness of their customers. Especially at Online credit providers, where there is no longer direct customer contact, these individual rating systems get a big boost Significance.

Um Trust to create, it is important that the financial service providers also work transparently on the subject of scoring. Informing customers about the composition, handling and processing of the data is important here. The benefit and importance of scoring can be explained in more detail in the customer meeting. Compliance with the relevant data protection regulations is also mandatory for the credit institutions.

Top books on the subject

Read text as PDF

Acquire this text as a PDF (only for own use without passing it on according to Terms and conditions): Please send us one after purchase eMail with the desired title supportberufebilder.de, we will then send the PDF to you immediately. You can also purchase text series.

4,99€Buy

Advice on success, goal achievement or marketing

You have Ask round to Career, Recruiting, personal development or increasing reach? Our AI consultant will help you for 5 euros a month – free for book buyers. We offer special ones for other topics IT services

5,00€ / per month Book

Book eCourse on Demand

Up to 30 lessons with 4 learning tasks each + final lesson as a PDF download. Please send us one after purchase eMail with the desired title supportberufebilder.de. Alternatively, we would be happy to put your course together for you or offer you a personal, regular one eMail-Course - all further information!

29,99€Buy

Skate eBook as desired

If our store does not offer you your desired topic: We will be happy to put together a book according to your wishes and deliver it in a format of yours Choice. Please sign us after purchase supportberufebilder.de

79,99€Buy

Here writes for you

Susanne Kleimst is an analyst and specialist journalist for the German-speaking area. She studied in Giessen and Berlin and now works as a freelance journalist in her adopted home, Stuttgart. Her main focus is on the areas of finance and insurance. All texts by Susanne Kleimst.

Popular Posts

-

3 X 5 tips for digital workflow: What does the future of work look like?

-

Further education financing: That costs further education and training

-

Job search & application for idealists & difficult cases: 5 tips for finding a job

-

False shame & modesty to prevent change: “What should the others think?”

-

Communication characteristics: Using the spirit of Olympia in everyday life!

-

Write advice texts: Always oriented to the reader

-

OPINION! Uwe Knaus, Daimler Blog Manager: "Dialog is the icing on the cake!"

-

Time management in everyday business: You score with punctuality

3 responses to "Loans & insurance for customers with risky occupations: Scoring as a protective factor"

-

Loans & insurance for customers with risk professions: Scoring as a protective factor by Susanne Kleimst ... - Recommended contribution A0L6TlsyES

-

Loans & insurance for customers with risk professions: Scoring as a protective factor for

Susanne ... via @ berufebilder - Recommended contribution OUeiiB2A9u -

Loans & insurance for customers with risk professions: Scoring as a protective factor for

Susanne ... via @ berufebilder - Recommended contribution irtlXq3Cw4

Post a Comment