More success stories?

Im Shop or our Newsletter you are guaranteed to find what you are looking for:

For their successful, good life Information you really need: Government-funded publisher, awarded the Global Business Award as Publisher of the Year: Books, Shops, eCourses, data-driven AI-Services. Print and online publications as well as the latest technology go hand in hand - with over 20 years of experience, partners like this Federal Ministry of Education, customers like Samsung, DELL, Telekom or universities. behind it Simone Janson, German Top 10 blogger, referenced in ARD, FAZ, ZEIT, WELT, Wikipedia.

Disclosure & copyrights: Text originally from: “Foreign exchange trading: Making money with exchange rate fluctuations” (2007), published by Münchener Verlagsgruppe (MVG), reprinted with the kind permission of the publisher.

By Dennis Metz (More) • Last updated on October 13.12.2023, XNUMX • First published on 18.07.2012/XNUMX/XNUMX • So far 4730 readers, 1416 social media shares Likes & Reviews (5 / 5) • Read & write comments

Since it Money there is also a need to exchange money from different origins (i.e. currencies) for one another. But the foreign exchange market has only existed in this form for a few years. A couple Basics.

A life without money is unimaginable today, as there is a multitude of Features fulfilled: It is a recognized medium of exchange, a unit of account with which goods and services can be compared, and a store of value.

Before "money" took on its current form, it had gone through several thousand years of development. The first means of payment dates from around 4500 BC. At that time silver was used as a means of payment. The first price lists were probably around 1500 v. BC used. Coins first appeared in the seventh century BC BC. In contrast to today's scraps, the precious metal content of the currency coins at that time corresponded to their face value. Paper money was probably invented in China in the ninth century, but it has only been used in Europe for around 300 years.

The foreign exchange market as it exists today has only existed in this form for a few years. Until not long ago, foreign exchange was traded in fixed relationships, which means that there was a fixed exchange relationship between two currencies. Flexible exchange rates, as are common today between the largest and most important currencies, have only been around for a few years.

The recent history of forex trading has its roots in the gold standard. With a brief interruption between the two world wars, this existed from around 1880 to 1939 System of the gold standard, a currency was backed by gold holdings. A banknote represented a claim to a certain amount of gold. This exchange ratio between money and gold was constant. Because the price of gold around Welt more or less identical, there were therefore also fixed exchange rates between the individual currencies.

The gold standard system collapsed in the course of World War II as a result of unfunded money augmentations. Banks issuing banknotes did not pass them on for surethat the money spent was covered by the corresponding amount of gold. Thus, the money supply grew while the gold supply remained constant.

The gold standard was eventually replaced by 1944 through the Bretton Woods Agreement. In this international system, gold was no longer used as collateral for a currency, but the US dollar. The participating currencies could be exchanged at any time in a fixed relation (+/- one percent) to the US dollar. Thus, the exchange rates between individual currencies were also fixed. US dollar holdings, in turn, could be exchanged for gold at a fixed rate (35 dollars per ounce). The gold-backed US dollar thus served internationally as the leading and anchor currency.

The BrettonWoods system has existed for over 25 years. In the course of the 60s, however, the US balance of payments deficit increased clear, and diverging growth rates between the participating countries created tensions. Finally, in 1961, the exchange rate between the German mark and the US dollar was adjusted for the first time, followed by a series of further adjustments at the end of the 60s. The system finally collapsed in the early 70s.

After a transition phase, the European Exchange Rate Association was finally founded. The system, also known as the »currency snake«, was characterized by close parities (+/- 2,5 percent) between the individual currencies within the European economic community. Exchange rates against the US dollar, on the other hand, were already flexible. The system only lasted until 1979 and was eventually replaced by the European Monetary System. There were no longer any fixed exchange rates between the European currencies, but fixed relations between the individual currencies against the fictitious currency basket ECU. The value of an ECU was calculated from the weighted average of a specified basket of currencies from the participating countries.

In the Maastricht Treaty, 1991 finally laid the foundation for the European common currency, the euro, which replaced the national currencies of the participating countries. The euro was finally introduced to 1999 and replaced the ECU. Since then, flexible exchange rates have prevailed among the most important currencies.

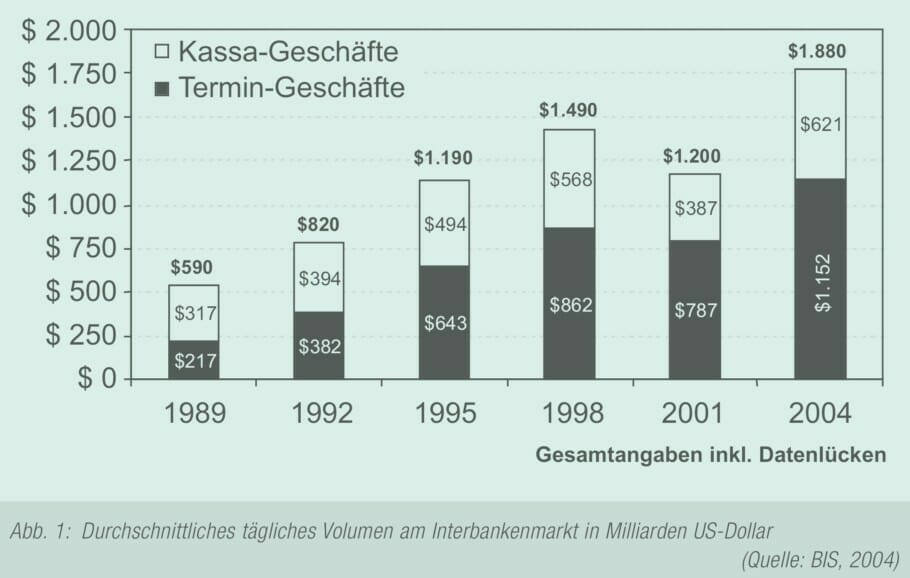

In the course of globalization, the volume traded has increased significantly in recent years. The average daily volume on the foreign exchange market was still around 1989 billion US dollars. This rose to an estimated 590 billion USD per trading day in 1.880. Hedge funds, among others, are held responsible for the strong increase since 2004. But the increasing perception of foreign exchange as an asset class has also supported the strong volume growth.

Within the banks there are a number of different groups that come into contact with foreign exchange transactions. These are primarily traders who actively trade foreign exchange. For example, they execute customer orders, act as market makers or trade on account the bank. But investment companies and hedge funds are now also major players in the foreign exchange market. Some of these also speculate on exchange rate fluctuations or at least need foreign exchange in order to be able to trade securities in foreign currencies. It can be seen that a large part of the volume is concentrated in fewer and fewer banks. In Germany, for example, only four banks are responsible for about three quarters of turnover on the foreign exchange market.

Central banks also participate in ordinary foreign exchange trading. However, central banks also intervene from time to time with the intention of moving the exchange rate in a certain direction and correcting a perceived market disruption. This is also known as intervention and usually results in a sharp movement in the exchange rate due to the market power of the central banks. Studies have shown, however, that these interventions are usually only temporary Success had.

The influence of classic (voice) brokers has decreased significantly in recent years, as more and more volume is traded via electronic trading platforms such as EBS. Especially when it comes to exotic currencies or large sums, the phone is still used, but in everyday trading the proportion of electronic systems is already an estimated 90 percent.

Although the share of real economic transactions cannot be determined beyond doubt, it is estimated to be a maximum of ten percent of the volume, with most sources assuming less than five percent. These transactions can largely be traced back to international groups. As part of globalization, large industries and service companies come into contact with a variety of currencies. Since goods and services are often billed in the local currency, the Companys increasing need for currency transactions.

The majority of all transactions on the foreign exchange market are not based on real economic processes and transactions, but are based on speculative motives. The foreign exchange market is dominated by some large commercial and investment banks, as well as central banks. Together they form the core of the foreign exchange market, which is presented in the following chapter 2.3.

One of the main differences between trading in for example shares and foreign exchange consists in the manner of trading. While stocks are usually traded on an exchange, currencies are traded over the counter (OTC). There is no marketplace that bundles supply and demand like a stock exchange, but the trading partners trade directly with each other. For example, if a bank wants to complete a foreign exchange transaction, it keeps calling other banks until it finds a trading partner for its transaction. Alternatively, it can also use one of the electronic brokers, which bundles at least part of the global supply and demand, but is not directly comparable to a stock exchange. The interbank market can thus be thought of as a Network imagine that connects the largest market participants with each other. If you are not part of the network, you need an intermediary (e.g. a broker, who in turn must be part of the network) to trade forex.

This results in a number of differences from trading on a stock exchange. For the private trader, this primarily consists of the trading hours. For example, trading in the interbank market is not subject to any time restrictions, such as those imposed by the trading hours on the stock exchange. Foreign exchange is traded around the clock - from Monday to Friday. Only on weekends does the retail stand still - although here, too, transactions theoretically come about when there are two trading partners.

![Background knowledge of professional liability: Liability risks for freelancers and self-employed [+ checklist]](https://e68zy2pxt2x.exactdn.com/wp-content/uploads/2013/haftungs-risiken.jpg?strip=all&lossy=1&ssl=1 "Background knowledge of professional liability: Liability risks for freelancers and self-employed [+ checklist]")

RT @AlmaMeise RT @SimoneJanson: Trends & dream jobs in the future tourism industry - Part 1: Culture, adventure travel &

RT @SimoneJanson: Trends & dream jobs in the future tourism industry - Part 1: Culture, adventure travel &

Trends & dream jobs in the future industry of tourism - part 1: Culture, adventure travel & sustainability #Business - Exciting contributionkz7LKoO

Trends & dream jobs in the future industry of tourism - part 1: Culture, adventure travel & sustainability #Business - Exciting contributionkz7LKoO

Trends & dream jobs in the future tourism industry - Part 1: Culture, adventure travel & sustainability: Sommerze ...

Trends & dream jobs in the future tourism industry - Part 1: Culture, adventure travel & sustainability ...

Post a Comment